THE KLTEC index has declined by 9.1%, underperforming the FBMKLCI, which has fallen 3.5% since the start of the year.

“The sharper drop in KLTEC is largely attributed to rising uncertainties surrounding the sector’s outlook, particularly after the AI chip diffusion, the emergence of DeepSeek, and escalating trade tensions,” said Kenanga Research (Kenanga) in the recent Thematic Report.

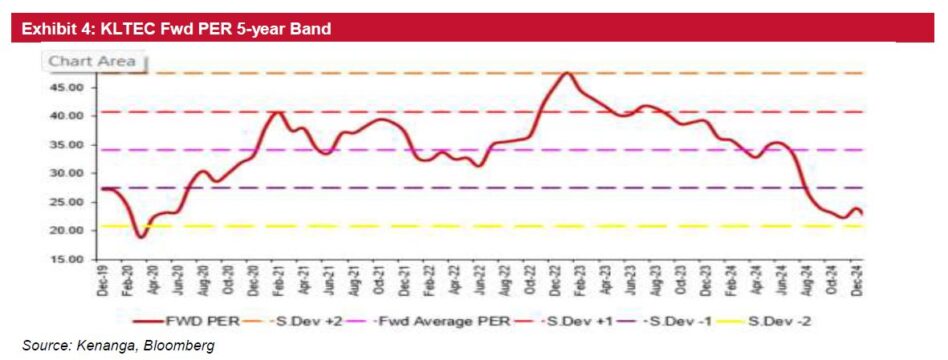

These concerns have led the KLTEC index closer to -2 standard deviations of its 5-year PER range, signaling a potential undervaluation.

The ongoing global semiconductor upcycle, driven by AI and high-performance computing (HPC), is expected to continue, albeit probably at a slower pace in the coming months as industry players reassess their business models in light of evolving market conditions.

Despite short-term volatility, there is a fair chance that the current global semiconductor uptrend—now in its 13th month— could extend beyond the typical 22-month cycle, albeit with a slower pace potentially.

This is primarily due to continued AI infrastructure expansion, which remains a key focus for industry players post-business realignment.

The current growth in the global semiconductor sector is underpinned by key structural drivers, including AI, HPC, 5G, and next-generation AI smartphone upgrades, which continue to fuel demand for advanced logic chips, GPUs, and AI accelerators.

The memory segment is experiencing strong tailwinds, supported by increased demand for DRAM and NAND flash in AI infrastructure, data storage, and 5G networks.

According to the World Semiconductor Trade Statistics (WSTS), the global semiconductor market is projected to grow by 19.0% year-on-year (YoY) to USD627bil in calendar year 2024 (CY24), followed by an 11.2% YoY increase to USD697bil in CY25, reinforcing expectations of a sustained industry rebound led by AI-related demand.

Persistent sector uncertainties are expected to keep volatility elevated and investor risk appetite subdued in the near term.

“Given this heightened volatility, we believe a NEUTRAL stance better reflects the current market environment. Re-rating catalyst would include trade tension tapering off or AI deployment visibility turns more concrete,” said Kenanga. —Feb 7, 2025

Main image: Pixabay