THE plastic manufacturing sector continues to face multiple headwinds including higher operating cost pressure, intensified competition but most of all, currency fluctuations and poorer calendar year 2025 (CY25) visibility due to global trade uncertainties from Trump’s tariffs.

“On the global front, demand for premium, thin-gauge or nano packaging film remained encouraging but demand growth for the plastic packaging sector as a whole is more mixed with average selling prices (ASP) weakening on both competitive pricing and domestic currency appreciation,” said Kenanga.

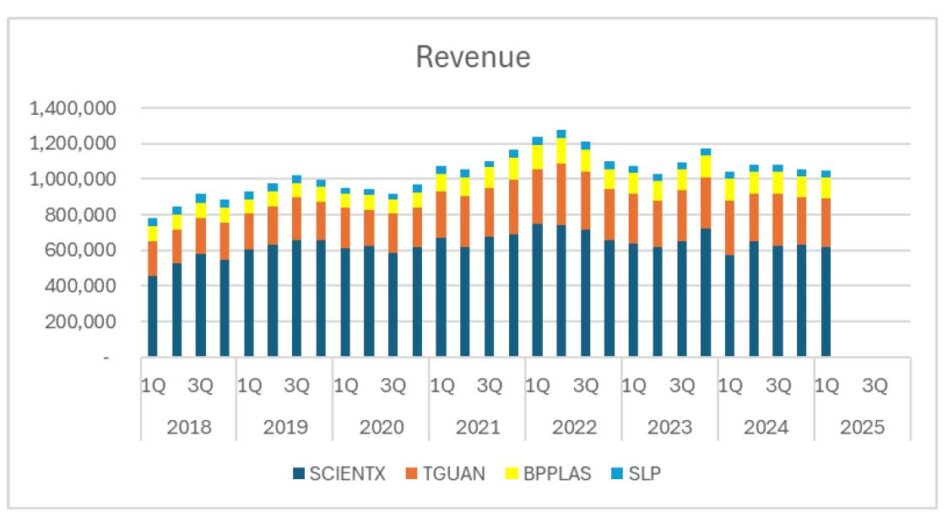

This trend is also reflective in the charts showing weaker PBT despite broadly stable revenues. Following our post-results analysis, and conversations with the industry players, we maintained our Neutral call, considering the following key factors:

Global Trade Uncertainties: We see greater indirect impact than a direct one (as the proportion of exports mix to the US from players we cover are below 5%) from the ongoing U.S. tariffs and global trade uncertainties.

A significant portion of plastic packaging films is used in B2B trades including inter-country trade to ease shipping and logistics; hence, a decline in global trade volumes is likely to have dampening effects by reducing overall consumption of plastic packaging materials produced by the companies under our coverage.

In addition to that, business owners around the globe may also hold back on inventory stocking activities due to the loss in confidence in global trades.

Competition: Since CY24, plastic players are faced with a challenging market not only due to slower global demand growth but intensified competition from overcapacity.

Part of this overcapacity arises as many local manufacturers often maintain their old facilities even after upgrading into e.g. new thin-gauge products.

This allows for very competitive marginal pricing for “old” packaging products.

Compounding this is some shifting in demand away from China by some American and European buyers which in turn compel Chinese players to offload stock at lower prices to other buyers such as those in SE Asia.

MYR Appreciation: In 1QCY25, the average USD/MYR exchange rate stood at RM4.45, compared to RM4.72 in 1QCY24, leading to some unfavorable forex translation for Malaysian plastic packaging producers.

That said, the MYR is on a strengthening trend, with Kenanga forecasting the average MYR rate to strengthen further to an average of RM4.25 in CY25 and RM4.08 in CY26, versus RM4.57 in CY24 (refer to Exhibit 2).

As such, the stronger MYR is expected to continue exerting pressure on average selling prices (ASP) and profit margins through forex translation effects. Based on general estimation, every 1% change in forex could impact 2%-3% of the sector’s profitability.

Rising Non-Resin Costs: Plastic manufacturers are facing additional headwinds from increasing non-resin operating costs, including higher minimum wages commencing this year and the upcoming electricity tariff hikes, which collectively could reduce local producers’ profitability by 5%-15%.

Meanwhile, resin prices in 1HCY25 were marginally lower by 3% YoY (refer to Exhibit 3). The combination of persistently high crude oil and resin supply, along with OPEC’s decision to further raise production, is expected to limit any significant near-term increase in resin costs.

Also, competition from both Chinese and local players is expected to persist and likely to further intensify moving forward.

On that note, we are adopting a more conservative sector-wide valuation approach, as we do not foresee a near-term re-rating for the sector. —July 15, 2025

Main image: Market Prospects