AFTER a strong CGPP award cycle in late calendar year 2024 (CY24), which lifted Hong Leong Investment Bank (HLIB) ‘s aggregate coverage orderbooks to RM1.4 bil.

The ongoing awards of LSS5 EPCC contracts has further lifted aggregate coverage orderbook to RM1.65 bil.

“As we had earlier highlighted, EPCC contract conversion for the LSS programme is seen to be significantly quicker than the CGPP programme leading to faster orderbook replenishment,” said HLIB regarding the renewable energy sector.

Meanwhile, continued robust take-up in the recently expired Net Energy Metering 3.0 (NEM 3.0) programmes help to sustain higher margin C&I project flows in respective orderbooks of solar players.

The SELCO programme will provide C&I players with an avenue to reduce electricity costs for the remainder of CY25.

We reckon the sector will continue to benefit from the pipeline of large scale of RE programmes like LSS5, LSS5+ (2GW), MyBeST and LSS6. We are estimating that potential EPCC value of RM10-15 bil assuming that LSS6 is 2GW.

Note that there is upside to such estimates since LSS6 could feature BESS integration. The slew of programme rollouts is expected to grow orderbooks in the RE segment over the next 12 months.

Adding to this, there is also 190MW FiT small hydro and bioenergy bids to be called later of the year and could translate into EPCC contracts for bioenergy players.

To this end, we view Solarvest’s target of hitting RM2 bil orderbook in FY03/26 as a conservative target; the company has consistently secured 30-40% share of large scale solar programmes.

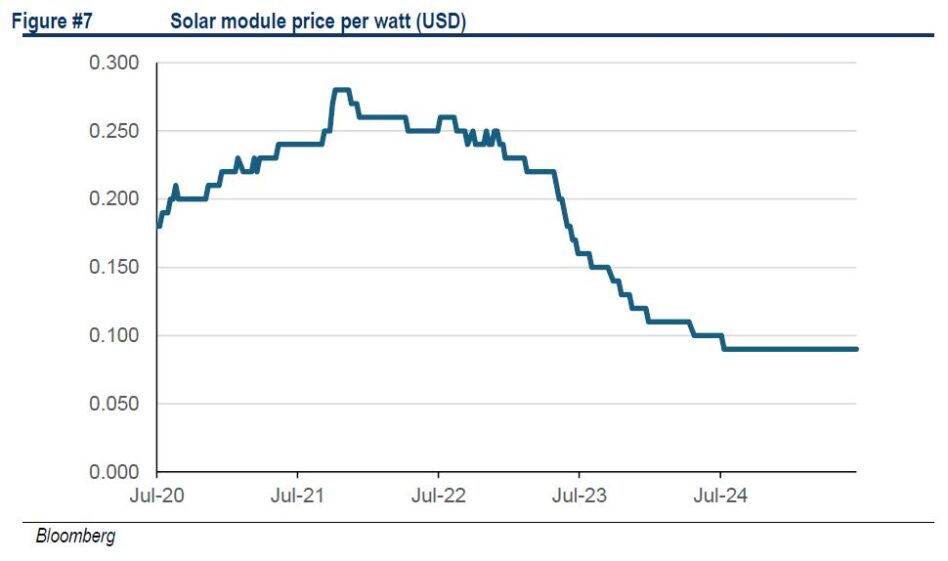

The solar module market remains sluggish with average selling price (ASP)s languishing sideways at ~USD9 cents/Watt, staying weak due to oversupply conditions.

We attribute such accommodative costs as key to rapidly declining LSS bid tariffs, estimated at an average of -22% since LSS4. Modules prices are expected to stay weak on the back of excess manufacturing capacity.

Along similar lines, BESS systems are also experiencing downward trending price per MWh, declining by -20% over the past year.

This enhances economics of BESS integrated solar deployments. Prevailing cost dynamics are strategic for government’s pursuit of NETR goals.

We make no changes to our overweight sector rating. We like the sector riding on strong structural themes as well as positive earnings growth cycle.

Key catalysts include contract rollout, CRESS, fresh RE quotas and export news flow. Risks: execution, slower-than-expected DC builds and cost pressure. —July 18, 2025

Main image: Getty Images