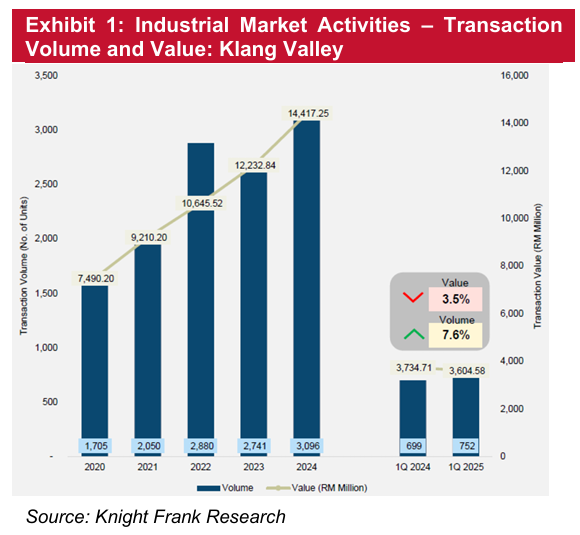

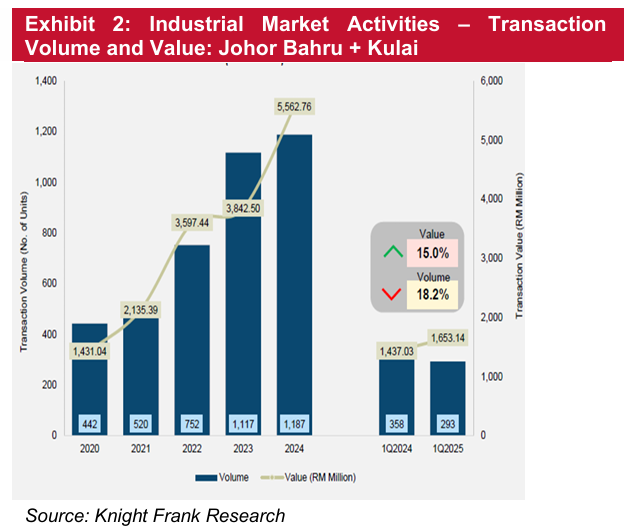

KNIGHT Frank found that between 2020 and 2024, annual industrial transaction values in Klang Valley and Johor Bahru grew by an 18% and 40% 4-year compounded annual growth rate, respectively.

While this could be attributed to pent-up demand coming out of the Covid-19 pandemic, it ties in with the increase of capital investments injected into the mentioned regions.

Kenanga opines that Klang Valley will likely remain the largest industrial hub in the country on the back of its relatively more mature industrial parks, infrastructure and strategic access to ports.

Specifically on Johor, Kenanga gathered that its industrial and data centre boom commenced with the launch of YTL Green Data Centre Park in Kulai in Aug 2022.

This kickstarted interests by large multinationals in the state, further fuelling its investments into that space.

Now, with the officiation of Johor’s SFZ in Sep 2024 and SEZ in Jan 2025, in addition to the increase in cross-border activities with Singapore stemming from the upcoming launch of the RTS, Kenanga believes that activities and investments into the state could remain buoyant in the near-to-medium term.

Penang remains a hot spot for industrial activity, mostly dominated by the technology and semiconductor sectors, Kenanga believes.

“However, we opine that sentiment within the state does appear to be highly cyclical with foreign investments appearing largely frontloaded, as highlighted by Knight Frank during the session via approved manufactruring investments data of the state,” said Kenanga.

According to Kenanga’s checks, the state government is looking to inject new supply via its Silicon Island project, south of Bayan Lepas, though visible spillover is yet to be seen in listed developers other than GAMUDA which is the joint developer.

Focusing on high-rise residential trends, Knight Frank highlighted that transaction volumes and values in KL had picked up mostly in 2022, coming out of the pandemic.

Knight Frank found it worth noting as well that the growth of average transaction values had outpaced volumes, reflecting a higher appetite by homebuyers for higher-priced homes.

From Kenanga’s checks among property developers and mortgage lenders, the pick-up in transaction volumes in 2022 could have been made up by more affordable offerings (RM300K−RM500K) which led market launches at that time, owing to development being stalled by movement control orders between 2020 and 2021.

Notably, MAHSING’s 3,700-unit M Vertica project saw its handover during this year, which may have prompted pent-up subselling of units.

Between 2023 and 2024, we noted the completion of several high-end residences such as Core Residences @ TRX, Agile @ Bukit Bintang and Pavilion Ceylon Hill @ Changkat with notable launches being Talisa @ Bangsar Hill Park, Branniganz Suites @ Bukit Bintang and Skyline Embassy @ Ampang.

In the lens of lenders, a higher value mortgage mix paints a better outlook for asset quality as high income/networth individuals are typically seen to have lower repayment risks, Kenanga observes.

We also witnessed that average mortgage loan approval rates were the highest in 2024 at 44.6% with May 2025’s monthly average coming in at 46.4%. This signifies an increasing willingness to lend in a property value appreciating environment. —Aug 6, 2025

Main image: Southgate Realty