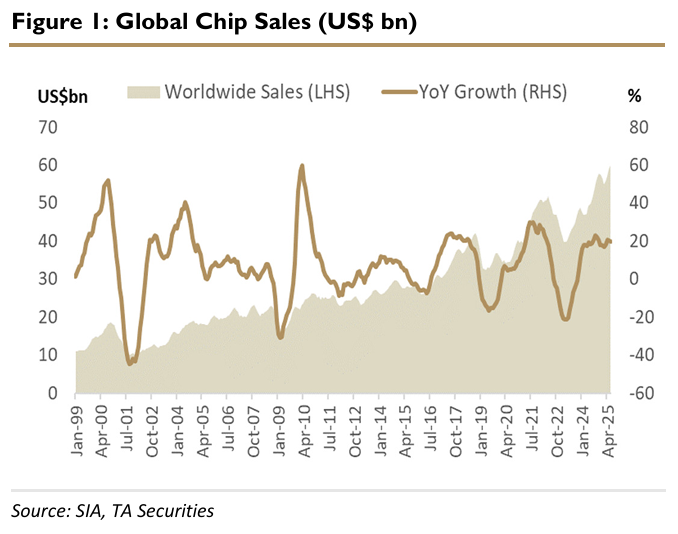

IN JUNE 2025, the global semiconductor sector sustained its positive momentum with another strong rise in sales. According to the Semiconductor Industry Association, global semiconductor sales for the month reached USD59.9 bil, marking the 20th consecutive month of year-on-year (YoY) sales growth.

This is driven by sustained demand for AI and high-performance computing applications.

The YoY improvement was primarily driven by all regions except Japan (-2.9% YoY). The Asia Pacific/All Other led the growth (+34.2% YoY), followed by Americas (+24.1% YoY), China (+13.1% YoY), and Europe (+5.3% YoY).

“Overall, the back-end equipment segment is anticipated to see continued growth in 2026, supported by the increasing complexity of device architectures and rising performance demands from AI and high-bandwidth memory applications,” said TA Securities.

Nevertheless, this growth is partially offset by ongoing softness in the automotive, industrial, and consumer markets.

According to US Commerce Secretary Howard Lutnick, the U.S. will soon announce the findings of a national security investigation into semiconductor imports.

To recap, the Department of Commerce previously initiated a Section 232 investigation to assess the potential risks that such imports may pose to national security.

Meanwhile, President Donald Trump has stated that the US will impose a tariff of around 100% on imported semiconductor chips, but exemptions will be granted to companies that have committed to manufacturing in the US.

We believe he is likely awaiting the outcome of the investigation before finalising the tariff rate and implementation framework.

In our view, any potential tariffs on semiconductor imports could significantly disrupt the global supply chain, given that the semiconductor industry is highly globalised.

The design, fabrication, testing and packaging activities are usually carried out across multiple countries.

The imposition of tariffs would raise production costs, some of which would likely be passed on to consumers, ultimately resulting in higher end-product prices and weaker demand.

Overall, we believe that more conditional exemptions will be announced over time, given the complexity and interdependence of the global semiconductor supply chain.

It would be extremely difficult for the U.S. to fully repatriate the semiconductor value chain in the near term, as building a self-sufficient ecosystem would take decades.

Despite the projected continued growth in global semiconductor sales, we maintain a cautious outlook due to lingering uncertainties surrounding U.S. trade policy.

On the other hand, we believe the Malaysian government will remain committed to implementing the National Semiconductor Strategy, with the aim of enhancing the country’s position in the global semiconductor value chain. Overall, we maintain our neutral stance on the semiconductor sector. —Aug 8, 2025

Main image: Shutterstock