DESPITE ongoing uncertainties due to the US tariffs, RHB believes aluminium prices will remain supportive amid the tight global supply, albeit offset by moderating demand.

“We remain positive on the outlook for aluminium smelters mainly due to easing alumina costs,” said RHB.

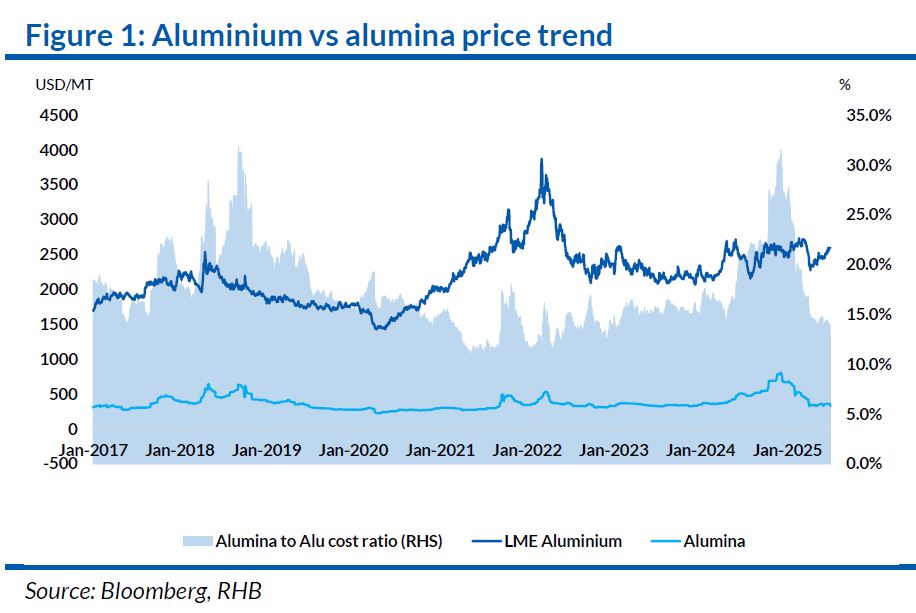

LME aluminium prices have been more volatile with the imposition of US tariffs, dropping to a low of USD2,300/tonne in April, but prices have since recovered to USD2,600/tonne.

While the tariffs have raised concerns on slower demand for aluminium, LME aluminium prices are supported as the overall global supply remains tight amid delays in the ramping up of new smelting capacity in Europe due to high energy costs, and limited room to grow in China as it nears the 45m tonne annual production cap.

That said, the Main Japanese Port (MJP) premium has fallen by 58% year-to-date (YTD) due to the higher supply in Asia following reduced interest in exporting to the US, whereas the US Midwest premium has risen 200% YTD.

On the cost side, alumina prices have decreased 46% YTD, accounting for only 14% of LME aluminium prices, down from a peak of 31% in Dec 2024, as supply chain disruptions from Guinea eased.

This bodes well for aluminium smelters, with a ramp-up in new refinery capacities in Asia.

In the longer term, we remain positive on PMAH as it targets increasing alumina self-sufficiency from 23% currently to c.99% by 2027, with the new refinery project in Indonesia.

Even if alumina prices fall further, Indonesia remains costcompetitive for alumina refineries due to its bauxite export ban.

Conversely, carbon anode costs have risen 23% YTD, driven by higher petroleum coke prices, following supply disruptions.

That said, margin should still be supported as carbon anodes make up a relatively small portion of smelting costs.

Last week, the Transport Ministry formally approved the scheme for MRT Circle Line, or also known as MRT 3.

Land acquisition is expected to be completed by end-2026, with contract awards and construction of the 51.6km line to begin in 2027.

We believe this will boost demand for cement in the midlong term, and anticipate LMC to be one of the biggest beneficiaries, given its huge market share of 60-70%.

Additionally, while LMC’s cement supply contract for the East Coast Rail Link Phase 1 ended in 2024, management guided that it is still supplying cement for Phase 2, albeit without an exclusive contract.

We note that bulk cement prices have remained stable at MYR380/tonne since Jul 2023, while coal prices have declined by 12% YTD, easing cost pressures for cement producers.

Key downside risks are rising input costs and a global slowdown, which could tamper construction activity and weaken demand for aluminium and cement. —July 23, 2025

Main image: Aluminium Online