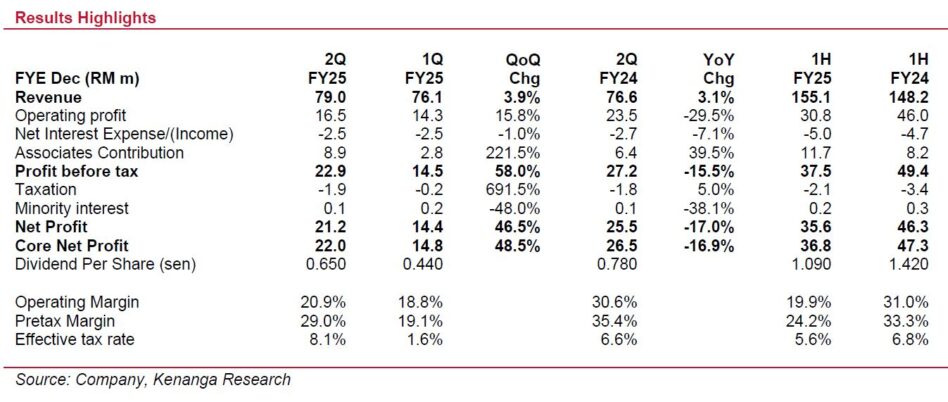

CTOS’s first half of financial year 2025 (1HFY25) core net profit of RM36.8 mil only made up 35% of Kenanga’s full-year forecast and 33% of consensus full year estimate.

The negative deviation was due to slower-than-expected revenues from Key Accounts and investment costs dragging gross profit margins. This is also CTOS’s third earnings cut for its FY25 guidance.

CTOS highlights favourable progress has been made regarding the hiring of a new CEO, which it is hopeful to announce by quarter four of calendar year 2025 (4QCY25).

Year-on-year (YoY), 1HFY25 revenue grew by 5% on the back of strong demand for digital products by CTOS’s Key Account segment. However, this was offset by fewer comprehensive portfolio reviews.

Operating profit declined by 33% as margin came off to 19.9% as cost of sales increased from lower margined international business alongside investment costs for new products which have yet to scale.

All in, excluding one-off rightsizing and shares-based expenses, this brought 1HFY25 normalised profit to RM36.8 mil (-22%).

Quarter-on-quarter (QoQ), 2QFY25 net profit surged by 49%, mostly due to stronger associate contributions (+222%) from better project flows by Juristech.

CTOS’s revenue streams remain in demand as the group boosts customer acquisition efforts across its key segments.

The group continues to grow its Key Accounts clientele and is working to develop a range of higher margin offerings to bolster profits.

Its commercial offerings may soon introduce value propositions concerning the digital fraud prevention space.

With regards to expenses, the group indicates that the higher investment costs incurred would dissipate by FY25.

At the meantime, its ongoing operational rightsizing exercise is anticipated to translate to cost savings of RM10 mil/year, to be completed by 4QFY25. This leans towards a better cost environment for FY26.

Still, as the group realigns its operations, it does not discount top line headwinds to spill over into FY26, which we opine could arise from customers lowering their frequency of use of CTOS’s products and solutions amid softening economic conditions in the near term.

With regards to FY27F’s absence of tax incentives, we project for the year’s net profit to come in flattish from FY26F revised net profit of RM102 mil. This is based on a 10% growth assumption to top line with margins remaining constant.

Kenanga downgrades CTOS to market perform. The group’s earnings shortfall may be a short-term conundrum as its long-term prospects could ride from an enlarged suite of products and eventual revitalisation of economic activity.

However, we note that the reversion to standard tax rates would also undermine its earnings accretion, which hampers a longer-term view with regards to dividend prospects. —July 28, 2025

Main image: CTOS